We’ll handpick the perfect real estate agent for your needs.

Today’s real estate market offers both challenges and opportunities. Whether you are interested in buying real estate, selling real estate, or finding foreclosures, we will connect you to a top local real estate agent who will help you fulfill all of your real estate needs. Best of all, our expert referral services are free to you, so you have nothing to lose, and everything to gain.

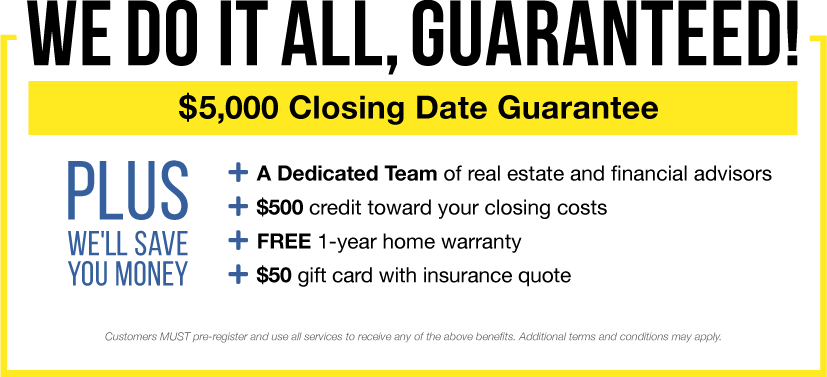

Using the wrong agent or trying to buy or sell yourself can cost you to lose thousands of dollars. Remove the guesswork and risk. Contact us today for a free, no obligation consultation with a pre-screened top-performing local Realtor.

Unlike other companies you may have seen, we don’t simply sell your information to the highest bidding agent. Agents can’t pay us to get leads, or to become part of our network. We personally work with you to understand your needs, and then handpick the best Realtor for you.

We’ll help you either sell your home or business property, or find a new home or commercial real estate for sale. Our real estate agents and Realtors from top local real estate brokers use the multiple listing service (MLS) to assist you with your real estate search or sale.

Use our free real estate tools to find home values, as well as find home mortgage rates and the best mortgage lenders.

WRA Realty.com will help you find a real estate agent from a top local real estate agency to act as your buyer’s agent, seller’s agent/listing agent, or general realty agent. WRA Realty.com is operated by Charles A. Kush III and Patricia Delgado, Licensed Referral Agents with Weichert Referral Associates Co. Inc., a member of the Weichert® Family of Companies.

Charles A. Kush III and Patricia Delgado

Licensed Referral Agents

Weichert Referral Associates Co. Inc.

Main Office: 1-800-937-6777

Direct: 330-732-5892 (330-REALTY-CO)

www.WRARealty.com

Contact us today for a free, no obligation consultation with a licensed top local real estate agent.